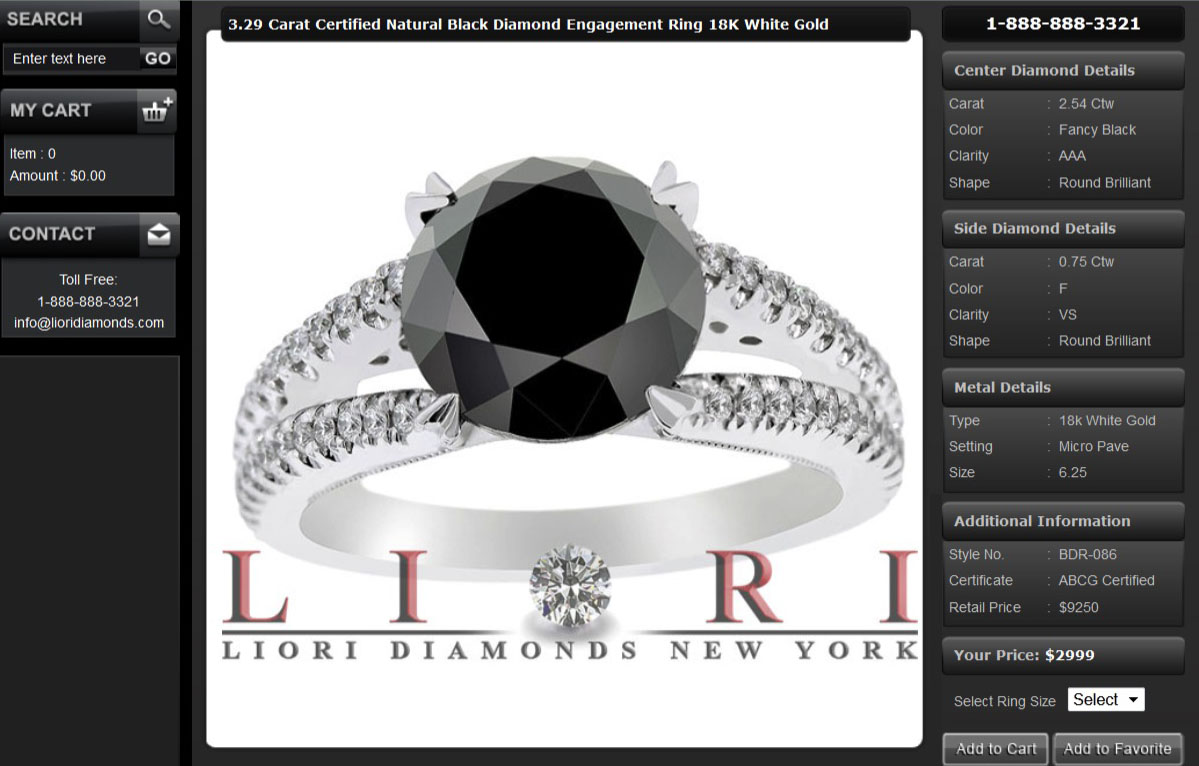

An insurer receives an application on a black diamond engagement ring. The appraisal values the ring at $9,250. The sales receipt says the buyer paid $2,999. Suspicious? Yes.

Here are some questions the insurer asked, and where the answers led.

Who wrote the appraisal?

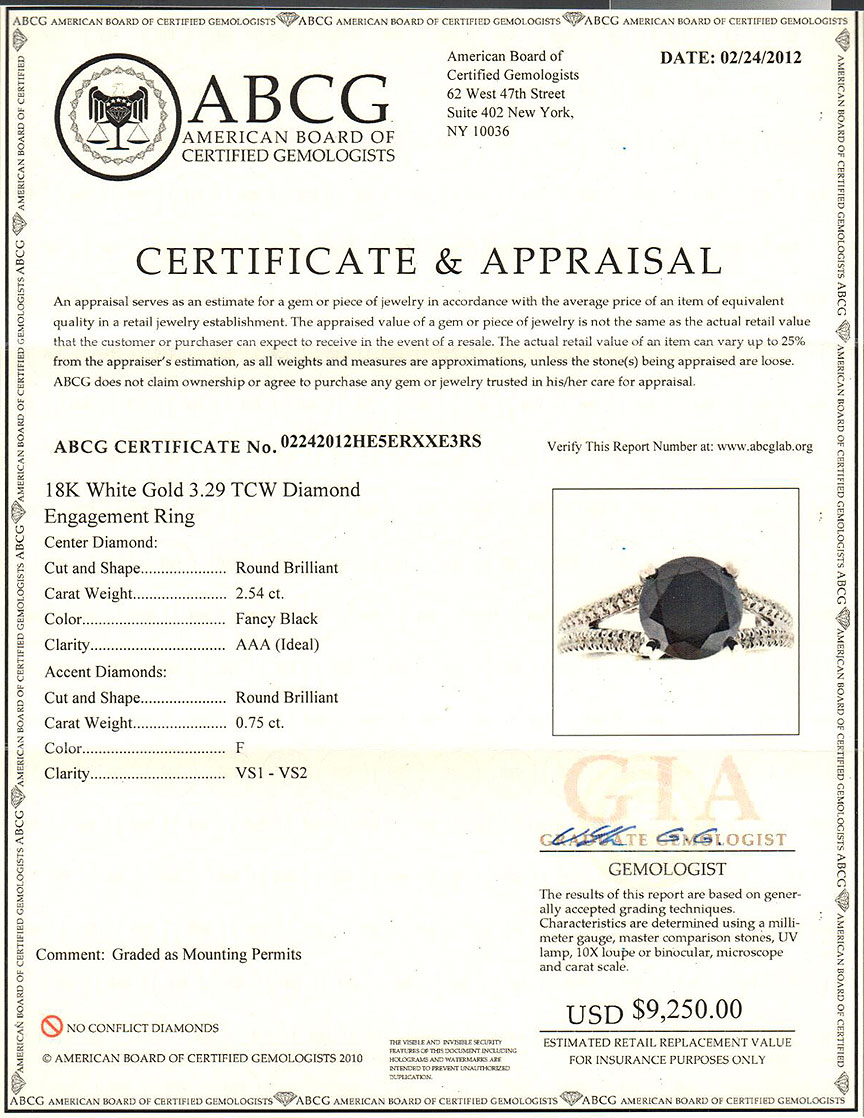

The submitted appraisal came from ABCG, American Board of Certified Gemologists.

The name sound official but . . . it’s just a name. The gemologists are not certified by anyone.

Who’s the seller?

Who’s the seller?

In this case, it’s an online retailer, Liori Diamonds. It has its own website as well as a strong eBay presence. In both places, similar rings were selling for under $3000.

So where did the $9,250 valuation come from?

Good question. It came from the seller’s desire to show the customer a document that “proves” the jewelry is a bargain, and the appraiser’s willingness to provide an inflated appraisal. A valuation more than 3 times the regular selling price is grossly inflated.

What about gem enhancements, or treatments?

The appraisal does not mention treatments — it does not specify whether the stone is treated or untreated. But on Yelp, the retailer has a promotion for the clarity enhanced diamonds it sells: “When you purchase a clarity enhanced stone [you are] purchasing the look of a VS stone for an SI price.” That is, the stone looks better than it is.

The appraisal does not mention treatments — it does not specify whether the stone is treated or untreated. But on Yelp, the retailer has a promotion for the clarity enhanced diamonds it sells: “When you purchase a clarity enhanced stone [you are] purchasing the look of a VS stone for an SI price.” That is, the stone looks better than it is.

The page on the Liori site carries the statement that the diamonds are natural and have not been treated or enhanced. We would like to see this statement on the appraisal. In fact, we’d like to see it on an independent appraisal not supplied by the seller.

Website text can be changed at any time. To the buyer, and to the insurer, it is the documents in hand that matter.

An enhanced stone is worth significantly less than an untreated stone of similar appearance (to the aided eye). So the insurer wondered whether the diamond on the jewelry in question was a treated, with a valuation of an untreated stone.

What’s the ring really worth?

When there is a huge difference between the appraised valuation and the purchase price, the selling price is a better indicator of true retail value. Valuation should be based on what the jewelry would sell for, and the purchase price is exactly that.

What are the appraiser’s credentials?

The ABCG website says all its appraisers are GIA Graduate Gemologists, and the document carries an illegible signature with GG behind it. We have no way of checking whether they’re GGs, but we have our doubts because . . .

What about the quality of the gems?

GIA has developed language for describing diamonds, terminology that is widely used and understood around the world. Although the ABCG graders are said to be GIA Graduate Gemologists, the grading on this document does not follow GIA standards.

On this certificate, “Round Brilliant” is used to describe cut and shape. But Round Brilliant is a term that designates only for the shape of the diamond. A diamond’s cut (one of the 4Cs, along with color, clarity and carat weight) is a set of proportions. Putting cut and shape together is just a way to obscure the fact that cut proportions are not being given at all.

On this certificate, “Round Brilliant” is used to describe cut and shape. But Round Brilliant is a term that designates only for the shape of the diamond. A diamond’s cut (one of the 4Cs, along with color, clarity and carat weight) is a set of proportions. Putting cut and shape together is just a way to obscure the fact that cut proportions are not being given at all.

Clarity is graded as “AAA (Ideal),” but this is a phony, feel-good phrase. GIA has no such grade. Its scale of grades goes from IF (internally flawless) to I3 (included 3). And “Ideal” describes the proportioning of a stone, not its clarity.

The color of the stone is said to be “Fancy Black,” but GIA has no such designation for color grade.

Such bogus grades tell us nothing. Unless the appraisal uses standardized grading terminology, the descriptions are useless in determining value.

The document is called a “Certificate & Appraisal.” What’s the significance of that double name?

This lab is taking advantage of the prestige associated with the term “diamond certificate.” The document looks official, and its layout mimics the look of a diamond certificate from a respected diamond grading lab.

However, a certificate from a respected lab, such as GIA, only describes (or “grades”) the stone. It is not involved in sales, and does not assign value to the stone or to the jewelry as a whole. Its grading certificates can be trusted because the lab has a reputation for accuracy and impartiality.

It’s true that anything can be called a certificate, but in this case the issuing lab is riding on the popularity of jewelry “certificates” of all kinds being perceived as authoritative testimonies of value. ABCG has no status as a diamond grading authority.

This document is just an appraisal. A poor one, at that, with an inflated valuation.

What does “the fine print” say?

Here’s how ABCG stands behind its appraisals:

The American Board of Certified Gemologists is not to be held liable for any discrepancy on the grade or appraisal results of any diamond or gemstone. Should you seek a different opinion, it is your responsibility to accept any quality or monetary differences between the reports. Should you find that the diamond or gemstone you received is not in accordance with the issued report; ABCG is not to be held liable.

(from the ABCG website)

Who’s being scammed?

Even though the appraisal may be misleading, if the consumer is happy with the purchase, and if he got what he paid for, what’s the problem? Here are a few of the problems:

- If the ring is insured at the inflated appraised value of $9,250, the policyholder will pay more in premiums than he should.

- If a loss occurs and a claim is made, the insurance company will be able to price a replacement at far less than $9,250. If we take the purchase price as retail, and the insurer can get the ring for about 20% below retail, the cash payout to the policyholder would be about $2,399.

A payout of that amount would leave the insured feeling cheated — not by the retailer that sold him the ring, but by the agent and the insurer. The insured might decide to move all his other business from the agent and the insurance company.

- If a settlement is based on the inflated valuation rather than the retail price, the insurance company would be grossly overpaying.

- Buyers of $3,000 engagement rings are not high-rollers. They are most likely young people, just starting out, who don’t have much money and are looking for a bargain. They are just being fooled.

How prevalent are grossly inflated appraisals?

VERY! This is not at all an unusual case. Especially for jewelry purchased on the internet, documents distributed by jewelry sellers are often canned appraisals and certificates from bogus labs, and they are not to be trusted.

ABCG’s site says: “Our Expert diamond gem analysis is recognized by all major insurance companies.” What this means is that insurance companies accept these inflated appraisals, as they do most appraisals, at face value. Insurers are not experts; they are fooled, just as consumers are.

Why hasn’t the prevalence of inflated jewelry appraisals been reported in the jewelry industry press??? Why haven’t we seen exposés on national television?

Perhaps because the problem is so commonplace.

So what did the insurer do, when presented with this inflated appraisal?

The company insured the ring at the purchase price. The insurer did not want to rain on the buyer’s parade by telling him he didn’t get a bargain. But sooner or later someone will tell him the true value of the piece.

Note: This article was prompted by a real-world insurance application, but it would be unethical to reveal private information received from a policyholder. As it happens, jewelry appraisal inflation is so common that we were able to find many, many examples on the Internet. This is only one.

Source:JCRS

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.